The Transition to Mid-Cycle

Despite recent bouts of volatility global equity markets continue to be resilient. The MSCI World Index is up 9.4% on a year-to-date basis and it is up 4.7% on a quarter-to-date basis. These are very attractive gains especially if they were converted into annualized figures. As we all know by now, the global economy has recovered from the COVID-induced recession at a much faster rate than what was originally expected. Global equity markets have reacted accordingly with the MSCI World Index up more than 80% from the bottom that was established in March of 2020. So where do we go from here?

Based on various observations, we believe that the global economy has transitioned from early cycle to the mid-cycle stage. In the year that followed the stock market bottom (March 2020), global equities exhibited classic early cycle behaviour. The factors that led the stock market during the first year of the recovery were very typical and included small caps stocks and equities with high betas, high leverage, and low quality. The sectors that outperformed were textbook early cycle winners and included retail, autos, materials, semiconductors, home builders, banks, and transportation. On a historical basis, the early stage of the economic cycle can last up to two years. However, in the current cycle the early cycle phase was much shorter than usual given the V-shaped nature of the global economy recovery. The recession of 2020 was a different kind of recession given that it was triggered by a global pandemic. It was not caused by the typical factors that cause recessions such as overheating or asset bubbles. This is very important because the consumer and global corporations went into the recession from a position of strength. This is one of the key reasons why the global economy generated a V-shaped recovery and one of the fastest economic rebounds in history. It’s also why we have transitioned to mid-cycle at a quicker pace than previous cycles.

Some of the signs that lead us to believe that we have moved beyond early cycle include the recent underperformance of small cap stocks, a rebound in quality stocks, and a sharp decline in highly valued stocks. As measured by the Russell 2000, small cap stocks have underperformed the S&P 500 by more than 10% since March. High quality stocks which lagged significantly in the first year of the new bull market have recovered substantially over the last 2 months. Finally, some of the speculative high-flying stocks have experienced sharp declines over the last several months. This includes stocks such as Peloton, Teladoc, and Tesla, just to name a few.

What should investors expect during the mid-cycle phase of the current economic cycle? While we expect economic growth to remain robust, we do expect more volatility in the stock market and an increase in inflationary pressures. This will lead to rising bond yields and eventually interest rate hikes from central banks around the world. This typically leads to a contraction in the Price-to-Earnings ratio for global stock markets. This may sound like bad news on the surface. However, what it likely means is more volatility but still positive gains for the global equity markets.

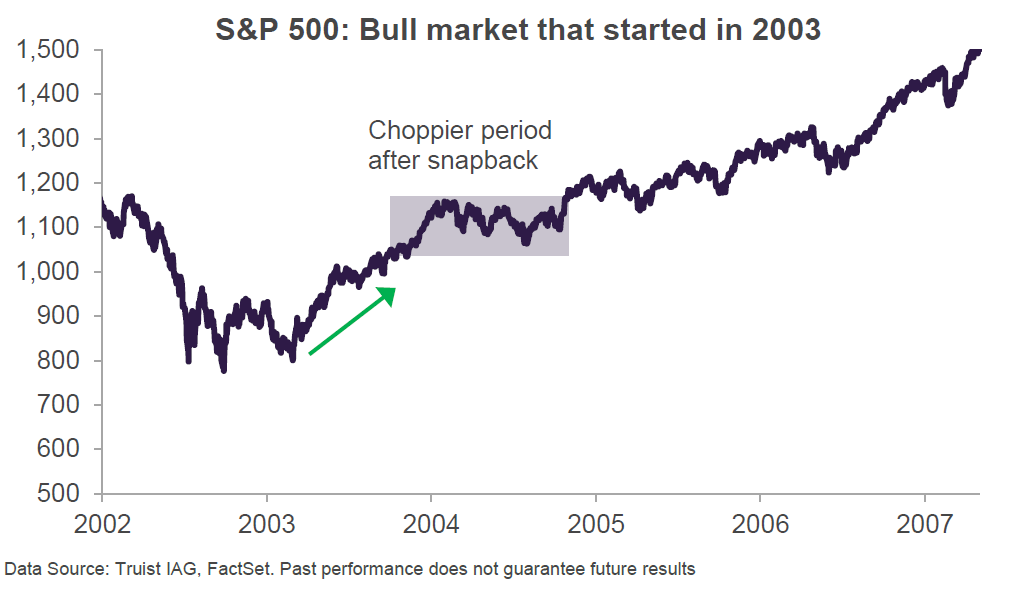

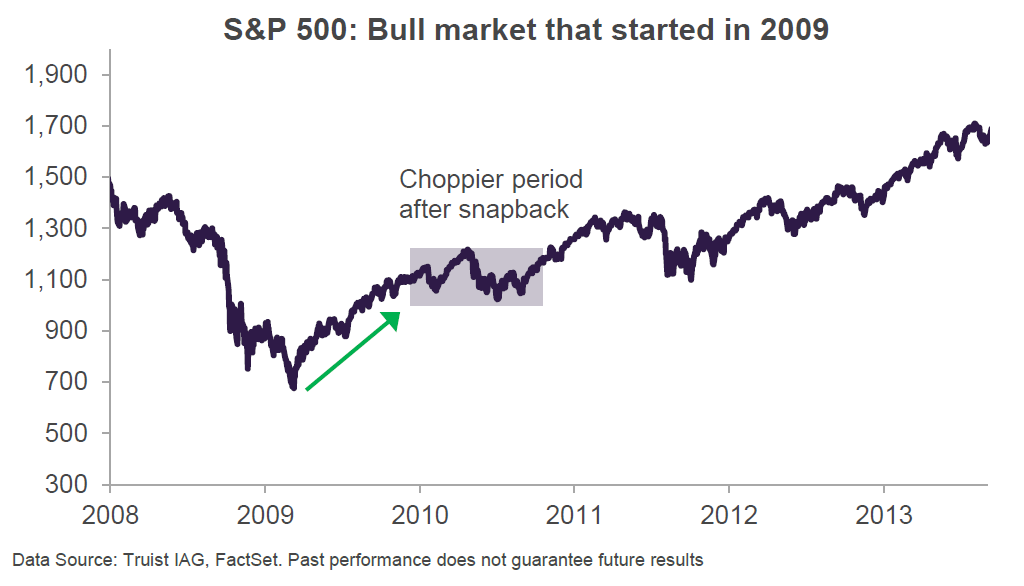

Looking back at previous market cycles can provide some context. In both 2003 and 2009, the S&P 500 generated substantial gains as the economy exited the recession. After the large snapback rallies, the S&P 500 moved to a choppier phase in 2004 and 2010 as seen in the chart below.

2004 and 2010 marked the second years of those respective bull markets. Despite the choppiness that ensued in both periods, the bull market in both time periods still had several years remaining. Although it is reasonable for investors to expect more volatility, stock market gains have typically been positive during the second year of a new bull market as seen in the chart below.

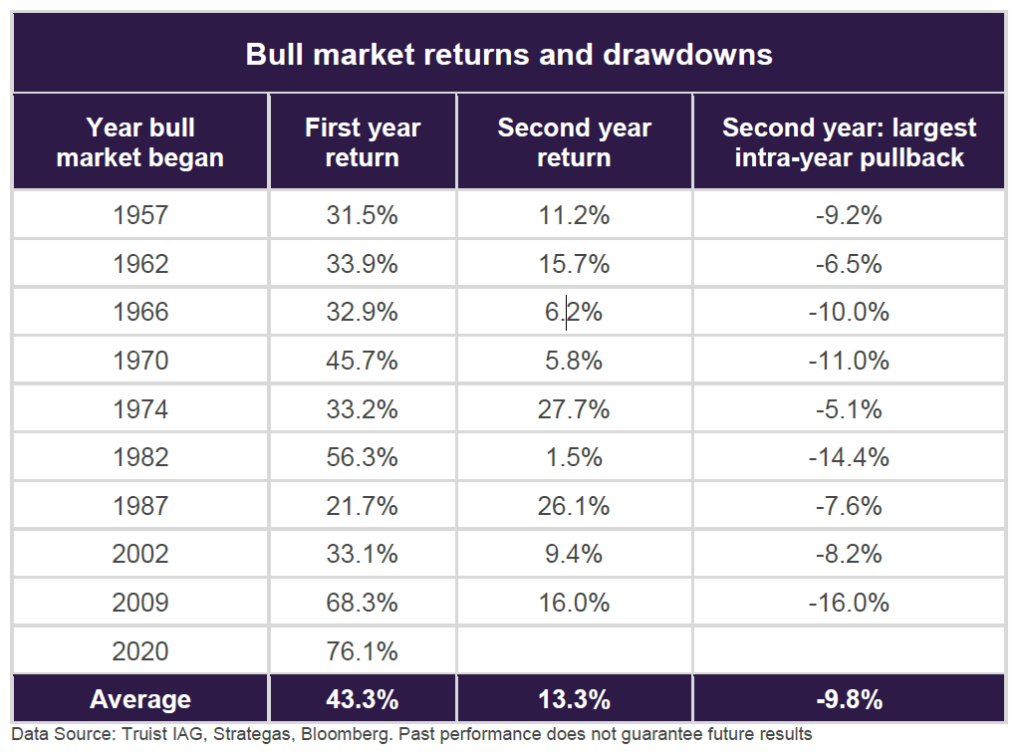

Based on data going back to 1957, the S&P 500 has generated an average return of 43.3% in the first year of a new bull market. During the second year of a new bull market the average return was 13.3%.

So how should investors position their portfolios for the mid-stage phase of the economic cycle? Given the expectation for rising inflation, we believe it is important to invest in companies with strong pricing power. These types of companies will be very well positioned as they can pass along rising input costs. Companies with pristine balance sheets will also be well positioned as they will be insulated from the impact of higher interest payments associated with rising interest rates. In addition, we believe it is important to avoid companies with elevated valuations. In an environment where Price-to-Earnings multiples are compressing, it is of paramount importance to avoid companies with unreasonable valuations. Our portfolios are constructed with high-quality companies that are highly profitable across the business cycle. The companies we own are resilient and many of them emerged from the COVID pandemic in an even stronger position than they were previously. Furthermore, our companies hold leadership positions in attractive industries which gives them strong pricing power. This will protect them as the global economy transitions to a higher inflationary environment. Our companies also have strong balance sheets and we believe they trade at reasonable valuations. In summary, we believe that our portfolios are very well positioned for the mid-stage phase of the economic cycle.

Have a good weekend,

Phil

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). NCM Asset Management Ltd. (NCM) is the Investment Fund Manager and CIC is the sub-advisor to the Kipling and NCM Funds. CIC is also the sub-advisor to certain CPWM investment mandates. This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. Reasonable efforts have been made to ensure that the information contained herein is accurate, complete and up to date, however, the information is subject to change without notice. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involved inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice and are provided in good faith but without legal responsibility. Past performance does not guarantee future results. CPWM and CIC may engage in trading strategies or hold long or short positions in any of the securities discussed in this communication and may alter such trading strategies or unwind such positions at any time without notice or liability. CPWM, CIC and NCM are under the common ownership of Cumberland Partners Ltd. Please contact your Portfolio Manager and refer to the offering documents for additional information.