The HALO Trade: Why Physical Assets Are Winning Over Software in 2026

Understanding the Shift from Digital to Physical

The investment landscape is undergoing a profound transformation. For the past decade, investors have favored “asset-light” companies—think software platforms and digital services that require minimal physical infrastructure. But in 2026, this preference is reversing dramatically. The market is now rotating toward “asset-heavy” industries: companies that own tangible infrastructure, physical networks, and hard assets that can’t be easily replicated.

This shift is called the HALO trade (Heavy Assets and Low Obsolescence), and it represents one of the most significant portfolio reallocations in recent memory.

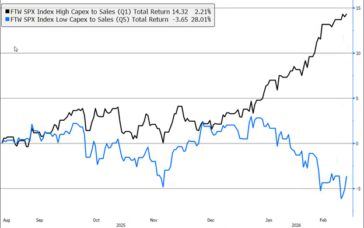

Performance of US Asset Heavy (High Capital Expense to Sales ratio) to Asset Light FTW SPX Stock Indices – Past 6 Months, August 2025 to February 2026

Source: Bloomberg. The above chart shows the outperformance in names that are asset heavy (high capital expense to sales ratio) versus companies that are asset light over the previous 6 months.

Why AI Changed Everything for Software Companies

The catalyst for this change is straightforward: artificial intelligence has fundamentally disrupted the software industry’s competitive advantage.

For decades, software companies enjoyed exceptional profit margins because building quality software required specialized talent, significant time investment, and deep technical expertise. These barriers to entry protected established players like Salesforce, Adobe, and ServiceNow from aggressive competition.

That protection is now gone.

Agentic AI—artificial intelligence systems that can independently write code, manage complex systems, and deploy solutions—has democratized software development. What once took a team of engineers months to build can now be generated by AI in days or weeks. The cost to launch a new software business has plummeted.

This creates a critical problem for established SaaS (Software-as-a-Service) companies: their historically high profit margins are now a target. AI-powered startups can undercut prices, replicate features faster, and compete on terms that were previously impossible. As competition intensifies, those attractive margins will inevitably compress.

The Market’s Response: Repricing SaaS Valuations

Investors are responding rationally to this threat. If software companies face margin compression and increased competition, their long-term profit potential—what analysts call “terminal value”—must be reassessed downward.

This is why we’re seeing valuation multiples compress for software and digital service companies. The market is essentially saying: “We’re less confident in your competitive moat.”

Meanwhile, companies with physical assets—power generation facilities, transportation networks, energy infrastructure, and manufacturing equipment—are gaining favor. Why? Because these assets have inherent protection:

- High replication costs: You can’t easily build a competing power grid or oil refinery

- Long technology cycles: Physical infrastructure remains relevant for decades

- Tangible value: Underground reserves, proprietary equipment, and global networks create genuine scarcity

The Irony: Tech Giants Become Capital-Intensive

Perhaps the most striking development is that the very companies that pioneered the asset-light model—Alphabet, Amazon, and Microsoft—have become the world’s largest capital spenders.

In 2026, these three hyperscalers are expected to invest approximately $500 billion in capital expenditures, representing roughly 32% of their combined sales. They’re building massive data centers, fiber-optic networks, and semiconductor facilities to power AI computing.

The message is clear: Even tech giants recognize that sustainable competitive advantage now requires physical infrastructure.

What This Means for Your Portfolio

The HALO trade reflects a rational reassessment of where value actually resides in the modern economy. Asset-heavy portfolios have significantly outperformed asset-light ones since early 2025, and this trend appears structurally sound.

For investors, this suggests:

- Diversification matters: Overweight positions in pure-play software may face headwinds

- Physical assets offer stability: Infrastructure, energy, and industrials provide tangible value protection

- The digital economy still needs physical foundations: AI and cloud computing require massive physical infrastructure—companies providing that infrastructure benefit from essential, hard-to-replicate assets

The rotation away from SaaS leadership toward physical asset ownership isn’t a temporary market whim. It reflects fundamental economic realities: in an era of abundant digital capacity and AI-driven competition, the assets that matter most are the ones that can’t be easily copied.

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involve inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice. Past performance does not guarantee future results.