Should we worry about the narrow breadth and market concentration in the S&P 500?

Over the last several years a lot has been written about the increasing power and concentration of Mega Cap stocks in the S&P 500. Media articles on this subject exploded in 2023 as Technology stocks skyrocketed and a new moniker was born when Bank of America analyst Michael Hartnett coined the term ‘Magnificent Seven’. For the record, the Magnificent Seven includes Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla. Apparently this term is a nod to a Western film from the 1960’s, which starred Steve McQueen as depicted in the picture below.

Does this exclusive group of seven stocks deserve all of the attention that it has received? In our opinion, the attention given to the Magnificent Seven is warranted when one considers the magnitude of the returns generated and the significant size that these stocks represent in the S&P 500 index.

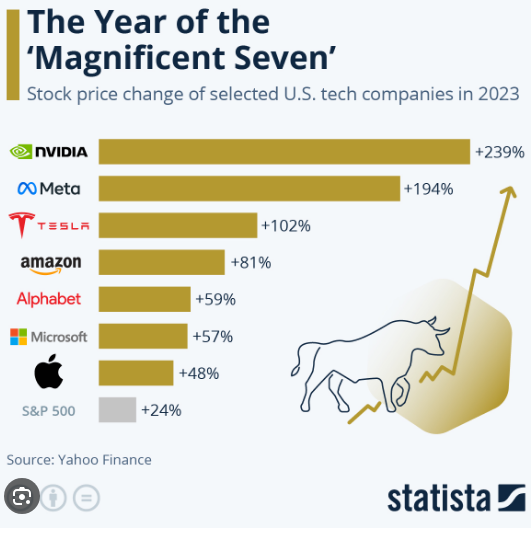

As seen in the chart below, the Magnificent Seven generated huge returns in 2023 including 3 stocks that increased in value by over 100%.

In terms of its contribution, the Magnificent Seven accounted for 62.2% of the S&P 500’s total return of 26.3% (in U.S. dollars) during 2023. Excluding the Magnificent Seven, the total return for the S&P 500 would have been significantly lower with the remaining companies in the index collectively generating a total return of 9.9% in U.S. dollars.

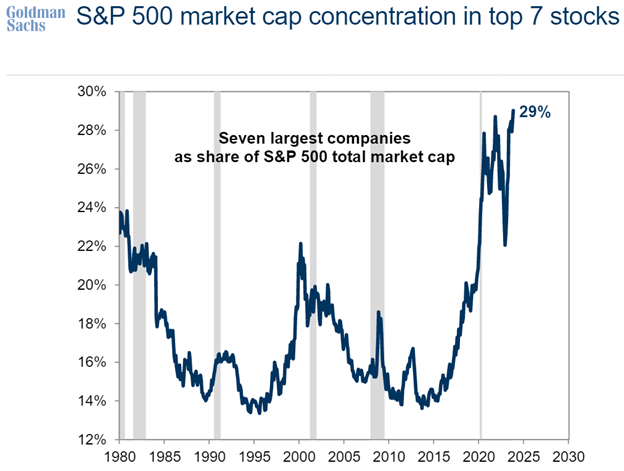

After the stellar performance of the Magnificent Seven in 2023, several concerns about market concentration have arisen. As you can see in the chart below, the Magnificent Seven collectively represent approximately 29% of the market capitalization of the S&P 500. This is the highest level for the largest 7 stocks in the S&P 500 over the last 45 years!

Given the magnitude of the market returns and the significant market concentration, a number of strategists have suggested that the recent returns of the Magnificent Seven are unsustainable. Some have even suggested that these stocks are in a bubble. We will only know the answers to these questions several years into the future with the benefit of hindsight. But for now, we ask ourselves the following question…is it unusual for a small group of stocks to generate the lion’s share of stock market returns? To put some numbers on this, let’s use 2023 as a starting point. During 2023, 1.4% of the stocks in the S&P 500 (The Magnificent Seven) generated 62.2% of the total return for the S&P 500. Fortunately, there are some academic studies that can help us compare the stock market returns generated in 2023 with market returns generated in the past.

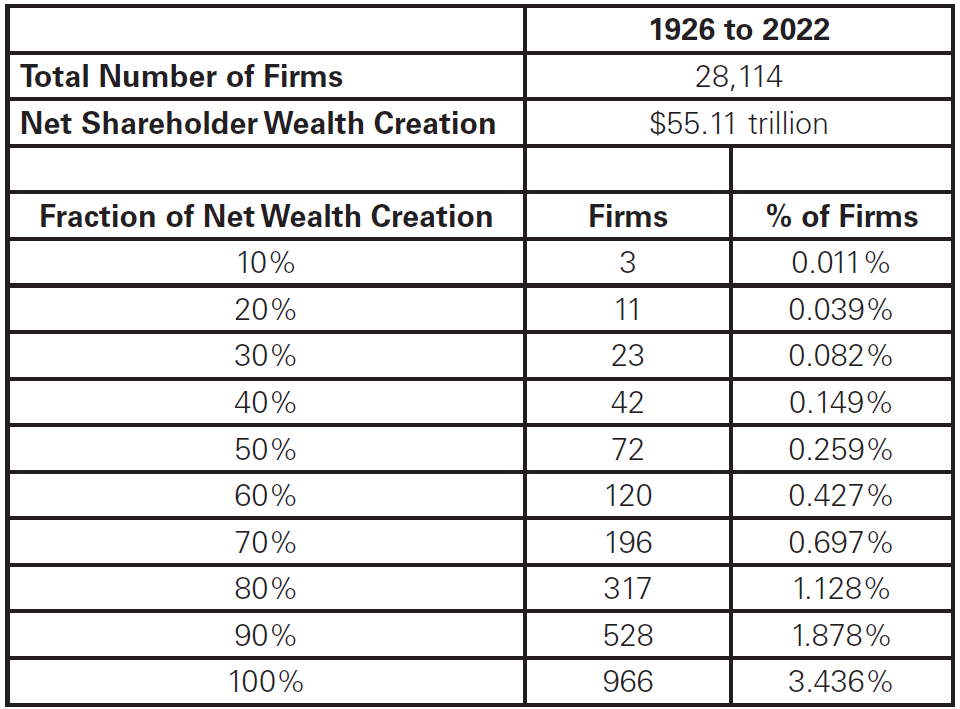

According to a study by Hendrik Bessembinder, history has shown that a narrow group of stocks has driven the majority of equity market returns over a long period of time. For the purposes of his study, equity market returns were defined as the excess returns generated by stocks over and above what could have been generated by investing in U.S. treasury bills. The study also refers to these excess returns as net wealth creation. The study included data from 1926 to 2022 and it included 28,114 publicly traded companies in the United States over this period. The output from this study confirmed that a very narrow group of stocks has generated the vast majority of net wealth creation over the period. To be more specific, 317 companies (or 1.1% of the stocks in the study) generated 80% of the total net wealth creation; 528 companies (or 1.9% of the stocks in the study) generated 90% of the total net wealth creation; and 966 stocks or (3.4% of the stocks in the study) generated 100% of the net wealth creation. These figures can be seen in the chart below.

When the results of this study are compared to 2023, the returns from the Magnificent Seven do not appear to be abnormal. In 2023, 1.4% of the stocks in the S&P 500 generated 62.2% of the total return for the S&P 500. Over 96 years (1926 to 2022), 1.9% of the stocks in the United States have generated 90% of the net wealth creation.

In conclusion, we don’t believe that there is anything unusual about the returns generated by the Magnificent Seven when taken in a historical context. There is no question that the Magnificent Seven generated spectacular returns in 2023 and it wouldn’t be surprising if this exclusive group of stocks experienced a period of weakness after generating supernormal returns in 2023. Having said that, we believe that it’s likely that some of these Magnificent Seven stocks will continue to create more value in the years ahead.

Sources:

Shareholder Wealth Enhancement, 1926 to 2022

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4448099#:~:text=Hendrik%20Bessembinder,-W.P.%20Carey%20School&text=Investments%20in%20publicly%2Dlisted%20U.S.,rather%20than%20increased%20shareholder%20wealth.

One chart shows how the ‘Magnificent 7’ have dominated the stock market in 2023

https://finance.yahoo.com/news/one-chart-shows-how-the-magnificent-7-have-dominated-the-stock-market-in-2023-203250125.html

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). NCM Asset Management Ltd. (NCM) is the Investment Fund Manager and CIC is the sub-advisor to the Kipling and NCM Funds. CIC is also the sub-advisor to certain CPWM investment mandates. This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involve inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice. Past performance does not guarantee future results. CPWM and CIC may engage in trading strategies or hold long or short positions in any of the securities discussed in this communication and may alter such trading strategies or unwind such positions at any time without notice or liability. CPWM, CIC and NCM are under the common ownership of Cumberland Partners Ltd. Please contact your Portfolio Manager and refer to the offering documents for additional information.