Pandemic to War

While writing this commentary, I learned that Russia initiated an official attack against the Ukraine. After Putin announced a special military operation through a televised address, explosions and gunfire were heard in Kyiv. The assault is being mounted by air, land, and sea, and it represents one of the largest attacks on a European state since World War Two. This is obviously a very sad situation and a difficult one given the hardships we have already suffered from fighting the global pandemic over the last 2 years. In terms of the impact, these types of regional conflicts have not had a significant impact on the global economy. People will continue to travel and businesses will carry on assuming this remains a regional conflict. Remarkably, these types of conflicts tend to have short-lived impacts on the stock market as we’ll discuss later in this piece.

After a very strong year in 2021, global stock markets have started this year on a very weak note. Both the MSCI World Index and the S&P 500 have declined by more than 10% from their highs. While this is disappointing for investors, stock market corrections have been a normal occurrence throughout history. In fact, over the last 30 years, the average annual peak to trough decline for the S&P 500 has been approximately 15%. In addition, it’s very typical for the stock market to eventually go through a period of consolidation after emerging from a recession. Looking back at previous market cycles can provide some context in this regard. In both 2003 and 2009, the S&P 500 generated substantial gains as the economy exited the recession. And this is exactly what happened in the economic recovery following the COVID-induced recession of 2020. The economic recovery has not only been one of the fastest on record, but it has also been one of the strongest recoveries from a stock market perspective. Both the MSCI World Index and the S&P 500 more than doubled in value from their March 2020 lows. And this happened in a span of less than 2 years, which is remarkable when you consider that average annual stock market returns have been in the high-single digit percentage range over the last 100 years.

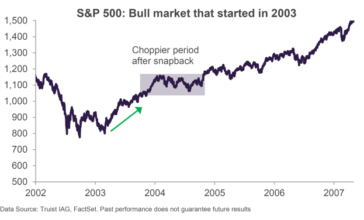

Throughout history, the stock market has typically generated outsized gains in the aftermath of a recession. This is what happened in the last 2 recessions that occurred in 2001-02 and 2008-09. However, after large snapback rallies, the S&P 500 moved to a choppier phase in 2004 and 2010 as the market consolidated its gains as seen in the charts below.

We believe the current market weakness that we have experienced thus far in 2022 is reminiscent of what happened in the last 2 downturns and almost every downturn that preceded those. The good news is that despite the choppiness that ensued in both 2004 and 2010, the bull market in both time periods still had several years remaining.

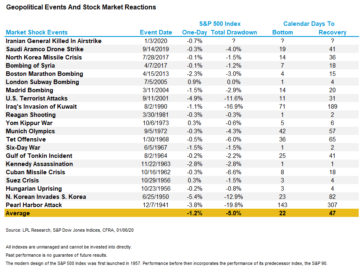

Returning to the situation in the Ukraine, stock markets tend to overreact to geopolitical events. After the Iraqi invasion of Kuwait in 1990, for example, the S&P 500 initially fell by 17% but later regained its previous high within about six months. While any military conflict is always a concern, the reality is that unless this develops into a much larger conflict, it is unlikely to be a long-term issue for the stock market. As seen in the chart below, geopolitical conflicts tend to have short-lived impacts on the stock market.

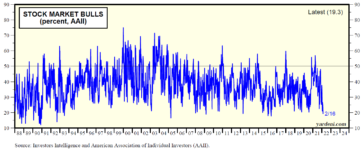

In terms of our actions, we are diligently looking for opportunities in the current market selloff and we believe it will prove to be a good buying opportunity for long-term focused investors such as ourselves. The level of bearishness in the stock market has increased significantly as per the surveys from the American Association of Individual Investors. This sentiment survey measures the percentage of individual investors who are bullish, bearish, and neutral on the stock market in the short term. As seen in the chart below, the current level of bearishness now (19.3% bullish) rivals the levels reached during the Great Financial Crisis (2008) and the height of the COVID Pandemic (2020). Both of these periods proved to be good buying opportunities.

From a contrarian perspective, we view this development as a bullish signal. When the AAII Bull/Bear Ratio has reached these depressed levels in the past, it has historically created an attractive buying opportunity. This doesn’t mean that the stock market can’t fall further in the near-term, but it does send a strong signal to us that we should be hunting for bargains.

Looking forward, we believe that stock market gains will moderate from the robust levels of the last 2 years and we expect there will be more volatility in the near term. Given the current level of uncertainty, forthcoming interest rate hikes, and the fact that we are moving later in the economic cycle, we believe that quality will become increasingly important. Companies with strong balance sheets that can generate substantial free cash flow throughout the economic cycle should be rewarded in the current environment, even if their stock prices have retraced some of last year’s strong gains in the year to date period. Investing in high quality companies is right in our wheelhouse so we are confident that our portfolios are well positioned for today’s stock market environment and as it evolves with the passage of time.

In summary and with the above said, the current environment is complex and there is much more to say. As such, we invite you to join a live meeting on Monday, February 28 at 4.30PM EST to hear more from our investment team about how we see the current situation unfolding, our portfolio positioning, and our current views on the market. We will also open the session to your questions at the end.

Have a great weekend,

Phil

Sources:

https://lplresearch.com/2020/01/08/how-stocks-do-during-geopolitical-events/

https://www.reuters.com/world/europe/putin-orders-military-operations-ukraine-demands-kyiv-forces-surrender-2022-02-24/

Yardeni Research

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). NCM Asset Management Ltd. (NCM) is the Investment Fund Manager and CIC is the sub-advisor to the Kipling and NCM Funds. CIC is also the sub-advisor to certain CPWM investment mandates. This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. Reasonable efforts have been made to ensure that the information contained herein is accurate, complete and up to date, however, the information is subject to change without notice. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involved inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice and are provided in good faith but without legal responsibility. Past performance does not guarantee future results. CPWM and CIC may engage in trading strategies or hold long or short positions in any of the securities discussed in this communication and may alter such trading strategies or unwind such positions at any time without notice or liability. CPWM, CIC and NCM are under the common ownership of Cumberland Partners Ltd. Please contact your Portfolio Manager and refer to the offering documents for additional information.