Let’s Talk About Inflation

In our recent conversations, a frequent topic of discussion has been around inflation. For the last few quarters, companies around the world have experienced rising input costs and tightness across skilled labour markets. Businesses are reporting difficulty with transportation and this has been exacerbated by the rising cost of shipping containers. Power outages, a shortage of truck drivers, and a large spike in the price of oil have also contributed to the current environment in which we find ourselves.

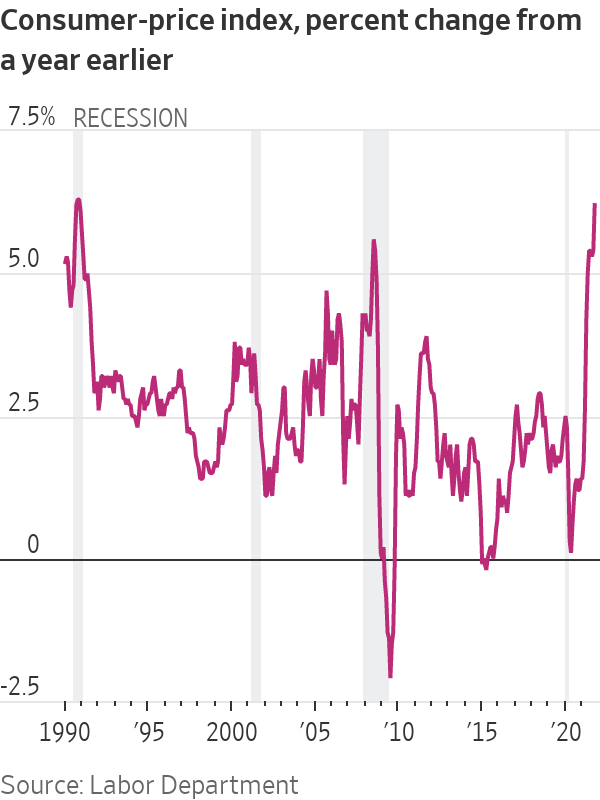

Are investors’ concerns surrounding inflation justified? We would say yes. As seen in this chart, U.S. consumer prices jumped in October at the fastest pace in three decades as inflationary pressures spread further throughout the economy.

The U.S. consumer price index (CPI) rose to 6.2% during the month of October. This represents the highest level since 1990 and it also marks a sharp increase from September’s level of 5.4%. While almost every single subindex was higher, the key drivers behind the rapid increase were energy, shelter, food, and new & used vehicles.

Policy makers prefer to focus on the core consumer price index which excludes the impact of food and energy costs, both of which can be highly volatile. However, even if we use the core CPI index, it tells us that U.S. inflation rate hasn’t been this high in 30 years. The recent core consumer price index measure was 4.6%, which is the highest level since 1991.

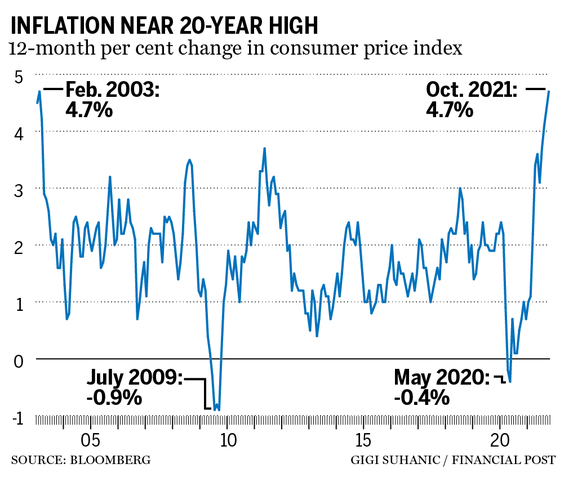

The inflation measures in Canada are somewhat lower but still concerning. As seen in the chart below, Canada’s consumer price index increased to 4.7% during the month of October.

Inflation is nearing its fastest pace since the Bank of Canada began using the consumer price index to set interest rates in the early 1990’s. The last time Canada’s consumer price index reached 4.7% was in February of 2003.

Economists and policy makers hope that inflation will be transitory, but the longer inflation lingers, the more likely it is that central banks will have to start raising interest rates and likely sooner rather than later. And perhaps at a faster rate than the market currently expects.

The question of whether inflation is transitory is important given that stocks have performed very well in the low interest rate environment that has existed for the last decade plus. Investors have coined the acronym TINA (There is No Alternative) to describe this phenomenon of investors paying higher prices for stocks than they have historically with low interest rates as the primary justification. However, if the stubborn bout of inflation persists, it will force central banks to raise interest rates. If this happens sooner and at a faster rate than the market is expecting, then investors may start to believe that TINA isn’t true anymore and they may gravitate towards bonds, which have less volatility. If this happens, it will spell trouble for stocks.

At the end of the day, the key question for investors is whether the current wave of inflation is transitory in nature or whether it will be longer lasting. Figuring out the answer to this question is very complicated given that there are so many different factors involved. To get to the bottom of this hotly debated issue, we need to answer a series of questions. Is the housing market strength sustainable, and if so, how long will it take for supply to catch up to this new level of demand? When will the COVID-enhanced unemployment benefits expire, turning today’s labor shortage into a labor glut? Will productivity surge in the aftermath of the pandemic due to new efficiency gains, thereby reinforcing the persistent and decades-long disinflationary pressures that have existed around the world? Will tensions between China and the United States result in a long-term move away from globalization, which has kept inflation under control for decades? Will the ruptured global supply chains be repaired in the next 6-12 months? Will high oil prices lead to demand destruction and ultimately cause a crash in oil prices just as energy producers decided it was a good time to increase their oil production?

These are very difficult questions and there are too many unknown factors making it very difficult to model future inflation with any degree of accuracy. So, if we can’t predict the rate of inflation into the future what should we do? The approach we have taken is to prepare for a wide range of scenarios. We believe that our portfolios have been constructed in a way that can hold up well in different types of economic backdrops including both inflationary and disinflationary environments. We believe the best way to accomplish this objective is to invest in high quality companies or what we like to call quality compounders. High quality companies have strong market positions, sustained pricing power, and seasoned management teams that can adapt to changes in the economic environment. In a higher inflationary environment, we believe that our companies will be well positioned due to their strong pricing power which will allow them to raise prices at least as fast as their costs and probably even faster. High quality businesses tend to have strong value propositions that enable them to pass on higher inflation to their customers. The ability to pass on higher inflation means that our companies can maintain or increase their expected future free cash flows in real, inflation-adjusted terms. In a disinflationary environment, we believe our companies’ pricing power will enable them to prevent their prices from falling as fast as their costs. We also believe that the dominant market positions and conservative balance sheets of our companies would allow them to survive and take market share from distressed competitors in a tougher economic backdrop.

In summary, we do not have strong views on the future level of inflation given the complexities involved in predicting the future rate of inflation. At a very high level, we believe that inflation will remain elevated in the short term. However, we also believe that many of the inflationary problems affecting the economy will get resolved over the medium term. When it comes to managing our portfolios, our positioning is not determined by a view on whether inflation will be transitory or not. Instead, we prefer to construct our portfolios with high quality companies that can perform well across a wide range of different economic environments.

Have a good weekend,

Phil

Sources:

https://www.wsj.com/articles/us-inflation-consumer-price-index-october-2021-11636491959

https://www.nytimes.com/2021/11/10/business/economy/consumer-price-inflation-october.html

https://financialpost.com/news/economy/canadas-annual-inflation-rate-hits-4-7-in-oct-highest-since-feb-2003

https://www.cbc.ca/news/business/inflation-u-s-october-1.6243781

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). NCM Asset Management Ltd. (NCM) is the Investment Fund Manager and CIC is the sub-advisor to the Kipling and NCM Funds. CIC is also the sub-advisor to certain CPWM investment mandates. This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. Reasonable efforts have been made to ensure that the information contained herein is accurate, complete and up to date, however, the information is subject to change without notice. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involved inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice and are provided in good faith but without legal responsibility. Past performance does not guarantee future results. CPWM and CIC may engage in trading strategies or hold long or short positions in any of the securities discussed in this communication and may alter such trading strategies or unwind such positions at any time without notice or liability. CPWM, CIC and NCM are under the common ownership of Cumberland Partners Ltd. Please contact your Portfolio Manager and refer to the offering documents for additional information.