Is the Recent Uptick in Inflation Transitory?

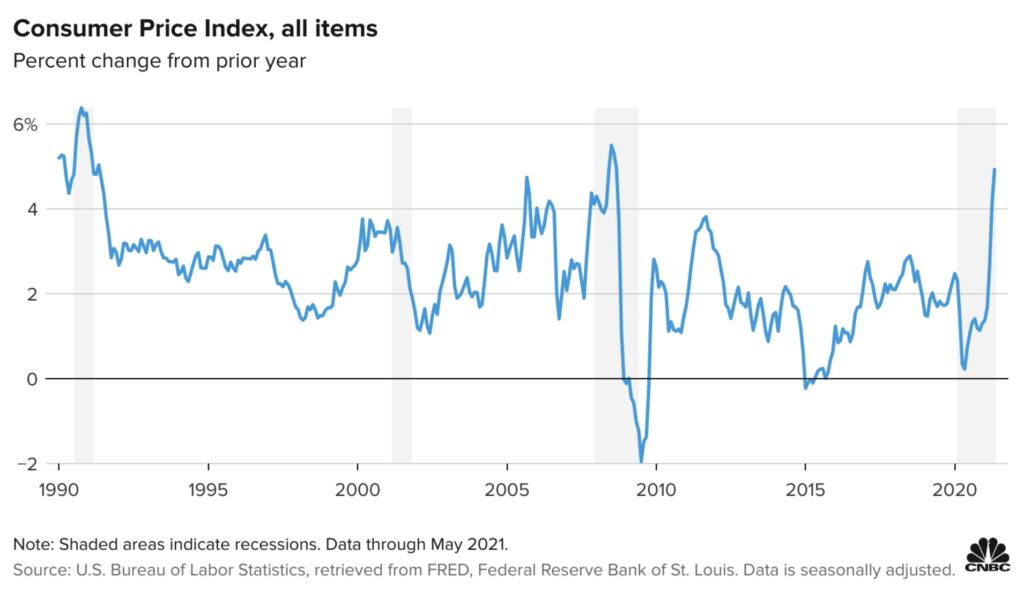

Based on our recent conversations, it is apparent that there is a major debate going on with regards to the rate of inflation and the sustainability of it. As seen in the chart below, inflation has soared in recent months and this has created some concern for investors.

During the month of May, the Consumer Price Index (CPI) rose by 5% compared to one year earlier. This was above the 4.7% rise that was forecasted by Economists and it marked the largest increase in the CPI since August of 2008. The Consumer Price Index is a closely watched measure and it represents a basket of goods including food, energy, housing costs, and sales across a spectrum of goods.

The key question as it pertains to this recent bout of inflation is whether it will be long lasting or whether it will be more transitory in nature. There are good arguments to be made for both cases and it is possible that both scenarios will prove to be correct over time. In the short term, there are good reasons to believe that inflation will remain stubbornly high. However, over the medium and long term these inflationary pressures should subside.

From our vantage point, the recent uptick in prices that is being felt by both businesses and consumers is largely driven by transitory disruptions that have occurred across various supply chains. These supply chains include food, semiconductors, oil, lumber, copper, shipping containers, and trucking. The supply shocks that are happening are an outcome of several factors that can be tied to the pandemic response. In the early stages of the pandemic there was a series of shutdowns that affected businesses across a wide range of industries. These shutdowns were made not only due to concerns about falling demand but also public safety measures that were implemented to contain the spread of the COVID virus. In hindsight, the magnitude of the shutdowns proved to be far too pessimistic. The shutdowns significantly underestimated the speed at which vaccines would get approved and the resulting rebound in demand. As a result of this, the demand side of the economy has rebounded faster than expected and the supply side of the economy has not been able to ramp up production fast enough to satisfy this demand. This helps to explain why we are now experiencing a spike in inflation.

It’s easy to see why there is an ongoing debate about inflation. The inflation bears can point to certain corners of the market that have already started to simmer down. Take lumber, one of the biggest gainers among commodities over the last year as Americans poured money into home remodeling. The price of lumber has collapsed by 40%1 since its peak in May. The booming U.S. housing market has also cooled as measured by building permits, which are a forward-looking indicator for home sales. For the month of May, building permits fell by 3.0%2 to just under 1.7 million units. This represented a seven-month low and the decline was widespread across regions and property types. Copper is another commodity that has eased from an all-time high. However, the inflation bulls can point to the numerous areas of the economy where supply constraints remain and torrid demand have left prices at multi-year highs. The answer to the inflation debate is that it can probably be found somewhere in the middle.

The hope that inflation will remain low forever and that interest rates will remain near zero forever seems unrealistic. This is especially the case given the communication that came out of the Federal Open Market Committee meeting this week. In a nutshell, The Federal Reserve raised its expectations for inflation this year and brought forward the time frame on when it will next raise interest rates.

On the other hand, we believe there is a low likelihood that the global economy will return to the high levels of inflation that occurred during the 1970’s and the 1980’s. The rationale behind this line of thinking is that there are several counter-inflationary secular trends that exist in the world today with Technology at the forefront of these trends. Technology acts as a counter-inflationary force in the global economy in several ways. Automation and robotics on the factory floor have improved productivity and lowered the cost of manufacturing. The rise of Ecommerce and the Internet has led to greater price transparency. This has resulted in greater price competition and has squeezed out high-cost producers across a number of global industries. Demographics is also a secular trend that provides a counter inflationary force for the global economy. The world is aging, people are living longer, and they are having fewer children. As people get into their 60’s and 70’s, they tend to spend less and become more frugal. An economy with aging demographic trends is likely to grow more slowly and generate less inflation.

So how should investors protect their portfolios given the prospects of rising inflation and higher interest rates? We believe that investing in high quality companies is the best way to insulate our portfolios given the expectation of higher inflation and rising interest rates. High quality companies typically operate in industries with high barriers to entry. This makes it difficult for new competitors to enter the market and typically enables the incumbents to earn above average returns on invested capital for extended periods of time. It also means strong pricing power and very stable cash flow generation. These attributes will protect them as the global economy transitions to a higher inflationary environment. In terms of higher interest rates, it means increased borrowing costs and reduced cash flows for highly indebted companies. High-quality businesses are somewhat insulated from this given that they are characterized by robust financial strength and consistent free cash flow generation. This reduces their dependence on debt capital and the negative impact to their earnings from higher borrowing costs.

In summary, we do believe that inflation will remain elevated in the near term but we do not believe that we are entering a period of substantially higher inflation like what was experienced in the 1970’s and 1980’s. Furthermore, we believe that our portfolios are very well positioned for the current environment given the high quality attributes of our investments.

Have a good weekend,

Phil

- Factset Data

- 2.CNBC

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). NCM Asset Management Ltd. (NCM) is the Investment Fund Manager and CIC is the sub-advisor to the Kipling and NCM Funds. CIC is also the sub-advisor to certain CPWM investment mandates. This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. Reasonable efforts have been made to ensure that the information contained herein is accurate, complete and up to date, however, the information is subject to change without notice. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involved inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice and are provided in good faith but without legal responsibility. Past performance does not guarantee future results. CPWM and CIC may engage in trading strategies or hold long or short positions in any of the securities discussed in this communication and may alter such trading strategies or unwind such positions at any time without notice or liability. CPWM, CIC and NCM are under the common ownership of Cumberland Partners Ltd. Please contact your Portfolio Manager and refer to the offering documents for additional information.