Is the Artificial Intelligence hype creating a bubble in Technology stocks?

There has been a lot of excitement about Artificial Intelligence (AI) recently and this is being reflected in the Technology sector, which has led the stock market thus far in 2023. AI is a transformative technology for consumers and enterprises, and one that will create new opportunities that will enhance productivity. Although AI has been around for a long time, it has only been used to perform narrow tasks such as voice recognition. However, the more recent excitement around AI is related to the opportunities related to Generative AI. One of the key attractions of Generative AI is the Large Language Models that are being developed. One of the distinguishing factors of Large Language Models is their deep understanding of language, allowing them to perform a wide range of language-based tasks. By utilizing Large Language Models, businesses will have access to state-of-the-art models that can be customized to leverage their own data.

We believe that AI technology is for real and that it will create significant opportunities for organizations around the world. While it is still early days for Generative AI, it won’t take long for the benefits to impact the global economy. Technology research company Gartner predicts that by 2025, more than 30% of new drugs and materials will be systematically discovered using Generative AI techniques, up from 0% today. Gartner also predicts that by 2025, 30% of outbound marketing messages from large organizations will be synthetically generated, up from less than 2% during 2022. Generative AI is expected to have an impact on a wide range of industries including pharmaceuticals, manufacturing, media, interior design, engineering, automotive, aerospace, defense, medical, electronics and energy. One of the key benefits of Generative AI is that it will enable enterprises to create new products more quickly. As companies incorporate AI models into their core processes, they will be able to improve the productivity of their marketing, design, and corporate communications activities.

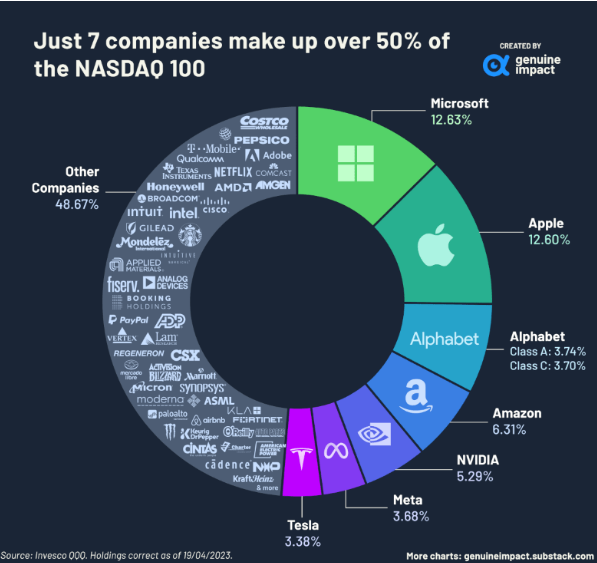

Given the huge run in AI related stocks, there are concerns that a Technology bubble is starting to form. And there is some data that one can point to if one wants to make an argument that a bubble is on the horizon. According to Goldman Sachs, hedge funds have increased their exposure to the seven biggest Technology stocks to the highest level ever seen. These 7 stocks include Tesla, Apple, Nvidia, Microsoft, Amazon, Meta and Alphabet. They have collectively been nicknamed the Magnificent Seven and they now make up more than 50% of the Nasdaq 100 as seen in the chart below.

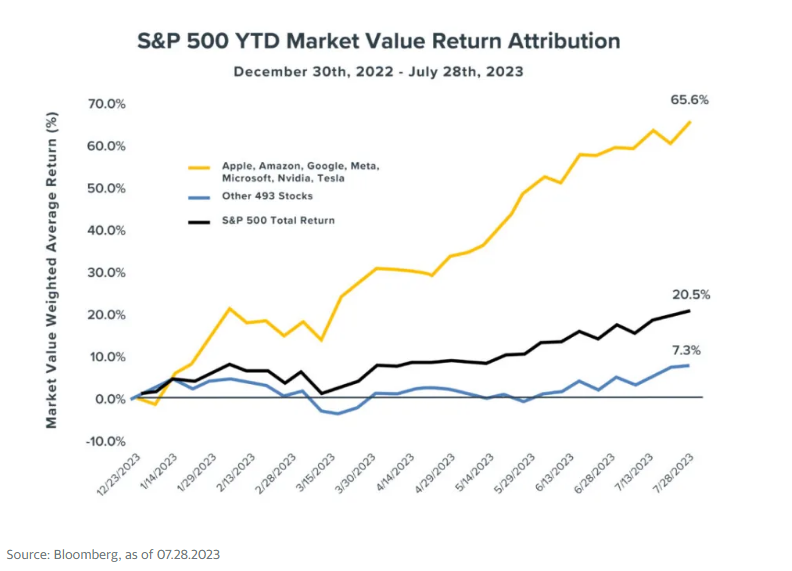

For those concerned about an AI bubble, one can also point to the outsized year-to-date returns generated by the Magnificent Seven compared to the rest of the S&P 500 as seen in the chart below.

In the first 7 months of the year, the Magnificent Seven soared by 65.6% as a group while the remaining 493 stocks in the S&P 500 gained 7.3% as a group. This implies that the Magnificent Seven have accounted for $4.5 trillion (or nearly 70%) of the S&P 500’s $6.5 trillion increase in market capitalization so far this year through to the end of July.

So are we in an AI bubble?

This is a good question, especially since many of us can remember the Dot.com boom in the late 1990’s, which ended with a 70% crash in the Nasdaq index. To address this question, we believe it makes sense to look at the individual stocks that make up the Magnificent Seven. Although some of the stocks in this group look expensive, some of them look very reasonably valued. On the expensive side, Tesla, and Amazon trade at a price-to-earnings (P/E) ratio of 54x and 43x, respectively, based on 2024 consensus estimates. While these multiples are lofty, they are lower than the 80x P/E ratio that was seen at the Dot.com peak in the late 1990’s. For the record, we don’t own Tesla and Amazon in our portfolios. On the more reasonable side, Alphabet (AKA Google) and Meta trade at a price-to-earnings (P/E) ratio of 20.0x and 17.5x, respectively, based on 2024 consensus estimates. These valuations appear attractive to us given the double-digit earnings profile of both companies. For the record we do own Alphabet and Meta in our portfolios. By looking at the individual stocks within the Magnificent Seven, we think it’s safe to say that some of the stocks within the Magnificent Seven are nowhere close to being in bubble territory.

So how are we playing the AI theme?

We own a number of stocks across our portfolios that will benefit from AI including language model developers, cloud service providers, and semiconductors. Meta has built a number of AI tools for developers including their open-sourced Large Language Models. Meta will also benefit directly from using their own models in their family of applications. Microsoft and Alphabet will also benefit from large language models and have much to gain from their cloud service offerings. Both Microsoft and Alphabet are building their platforms to enable their customers to train and deploy their models in the cloud. This will lead to an explosion of customized Large Language Models (LLM’s). Given their complexity and their size, these LLM’s will need to be stored and run in the cloud. We believe this puts Microsoft and Alphabet in a very favourable position. Within the semiconductor industry, we own several companies including ASML and Applied Materials. Given the large wave of data and computational power that will be required in the years ahead, we believe that the semiconductor industry is very well positioned to benefit from AI. In order to develop AI models, very large sets of data will be utilized in the training phase. The initial sets of data as well as the subsequent generation of new information will require semiconductor chips to perform computations and to store information. As demand for AI models grows exponentially, it will require significant gains in power efficiency. All of this will drive demand for the leading-edge chips, which is why we view the semiconductor industry as critical enabler for AI.

While there has been a tremendous amount of hype around Artificial Intelligence, we don’t view it as a bubble. We believe that AI will create significant productivity gains for the global economy in the years ahead so we don’t believe this is a fad that will disappear over time. In terms of getting exposure to the AI theme, the companies we own have very strong core businesses that were growing and highly profitable before the recent hype around Generative AI came along. While we believe the above-mentioned companies are very well positioned to benefit from AI, they have multiple avenues for growth outside of Artificial Intelligence.

Phil

Sources:

Gartner – Gartner experts answer the top generative AI questions for your enterprise

https://www.gartner.com/en/topics/generative-ai

UBS Q-Series – Will Generative AI deliver a generational transformation?

Are The “Magnificent 7” Tech Stocks Ready to Share the Road?

https://finance.yahoo.com/news/magnificent-7-tech-stocks-ready-182446058.html

Charted: Companies in the Nasdaq 100, by Weight

https://www.visualcapitalist.com/cp/nasdaq-100-companies-by-weight/#:~:text=Just%207%20Companies%20Dominate%20the,C%20shares%20occupying%20two%20spots.

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). NCM Asset Management Ltd. (NCM) is the Investment Fund Manager and CIC is the sub-advisor to the Kipling and NCM Funds. CIC is also the sub-advisor to certain CPWM investment mandates. This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. Any comments, statements or opinions made herein are those of the author and do not necessarily reflect those of Cumberland Private Wealth Management Inc. (Cumberland) and are not endorsed by Cumberland. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involve inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice. Past performance does not guarantee future results. CPWM and CIC may engage in trading strategies or hold long or short positions in any of the securities discussed in this communication and may alter such trading strategies or unwind such positions at any time without notice or liability. CPWM, CIC and NCM are under the common ownership of Cumberland Partners Ltd. Please contact your Portfolio Manager and refer to the offering documents for additional information.