Climbing The Wall of Worry

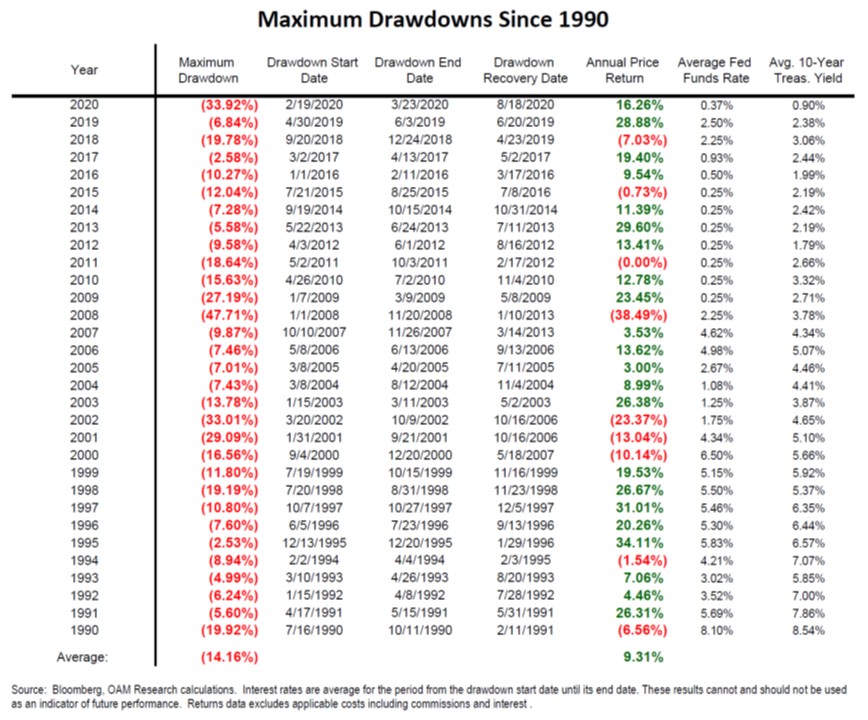

Global equity markets have been volatile over the last week with stocks meandering back and forth between positive and negative territory. After a huge run in the stock market over the last year, it is reasonable to expect a period of consolidation although the timing of this is uncertain. As seen in the chart below, the average annual drawdown from peak to trough was 14.2% over the last 40 years.

Over the last year the stock market has done a very fine job of climbing the so-called wall of worry. Going forward, the market will have to continue to do so because there is always a of list of worries for investors to fret about. At the current moment, the list of concerns includes rising interest rates, a spike in COVID cases, inflationary pressures, and a likely tax hike for U.S. Corporations. In addition, there are numerous signs of speculation including margin debt at all-time highs, investment sentiment readings showing extreme levels of optimism, and companies with no earnings finding their way into the public markets using SPAC’s (Special Purpose Acquisition Corporations). What should a rational investor do in the current environment? We will revisit this question in a moment. But first, let us consider what the experts are focused on.

In recent months, it appears that market strategists and economists are spending an increasing amount of time trying to make predictions about the U.S. 10-year Treasury Yield, the US dollar, the level of economic growth, and the forthcoming inflation. These predictions are then used to determine ‘the best trades’ for investors such as the decision to be invested in value or growth stocks. We don’t try to make predictions about the 10-year Treasury Yield or the inflation rate, nor do we spend much time thinking about the narrative on growth versus value stocks. We don’t believe it is easy to execute a strategy based on forecasting the twists & turns of the global economy and then re-adjusting the portfolios accordingly. When it comes to the debate on growth versus value, we don’t spend a lot of time thinking about it. One of the key issues with the ongoing debate about growth and value is that the term ‘value’ means different things to different people. This has created confusion over the years. In his 1992 letter to shareholders, Warren Buffet shared some interesting perspectives on the growth versus value debate.

“Most analysts feel they must choose between two approaches customarily thought to be in opposition: “value” and “growth.” Indeed, many investment professionals see any mixing of the two terms as a form of intellectual cross-dressing. We view that as fuzzy thinking (in which, it must be confessed, I myself engaged some years ago). In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive. In addition, we think the very term “value investing” is redundant. What is “investing” if it is not the act of seeking value at least sufficient to justify the amount paid? Consciously paying more for a stock than its calculated value – in the hope that it can soon be sold for a still-higher price – should be labeled speculation.”

So, what should a stock market investor do in the current environment? We don’t believe there is a ‘right’ answer but this is what we are doing. We follow a consistent investment philosophy that has been in place for many years. In a nutshell, we build concentrated portfolios with high quality companies and we use a long-term investment horizon. We are looking for companies that are run by experienced management teams with a history of prudent capital allocation. We invest in corporations that have a competitive advantage or a protective moat around their business. By doing this, we end up with a portfolio full of companies that operate in industries with high barriers to entry. This makes it difficult for new competitors to enter the market and typically allows our companies to earn above average returns on invested capital for extended periods of time. These types of companies typically generate robust free cash flow and can do so across the business cycle. High quality companies tend to hold up well during periods of market weakness given the stability of their earnings. Our portfolios held up well during the market panic of 2020 and we believe they will do so again when the stock market goes through the next phase of market weakness.

Have a good weekend,

Phil

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). NCM Asset Management Ltd. (NCM) is the Investment Fund Manager and CIC is the sub-advisor to the Kipling and NCM Funds. CIC is also the sub-advisor to certain CPWM investment mandates. This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. Reasonable efforts have been made to ensure that the information contained herein is accurate, complete and up to date, however, the information is subject to change without notice. Information obtained from third parties is believed to be reliable but no representation or warranty, express or implied, is made by the author, CPWM or CIC as to its accuracy or completeness. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involved inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice and are provided in good faith but without legal responsibility. Past performance does not guarantee future results. CPWM and CIC may engage in trading strategies or hold long or short positions in any of the securities discussed in this communication and may alter such trading strategies or unwind such positions at any time without notice or liability. CPWM, CIC and NCM are under the common ownership of Cumberland Partners Ltd.