Climbing The Wall of Worry

It’s that time of year when investors get a little bit more nervous than usual. September is historically known as a turbulent month for the stock market and a time when accidents can happen, so to speak. It’s not just a case of seasonality that has investors worried, there are a bunch of different factors that are weighing on their minds. Peak economic growth, peak earnings growth, inflation, the U.S. debt ceiling, Fed tapering, the Delta COVID variant, the efficacy of the vaccines, China’s economic slowdown, Evergrande, and supply chain disruptions around the world. These are some of the concerns, otherwise know as the Wall of Worry.

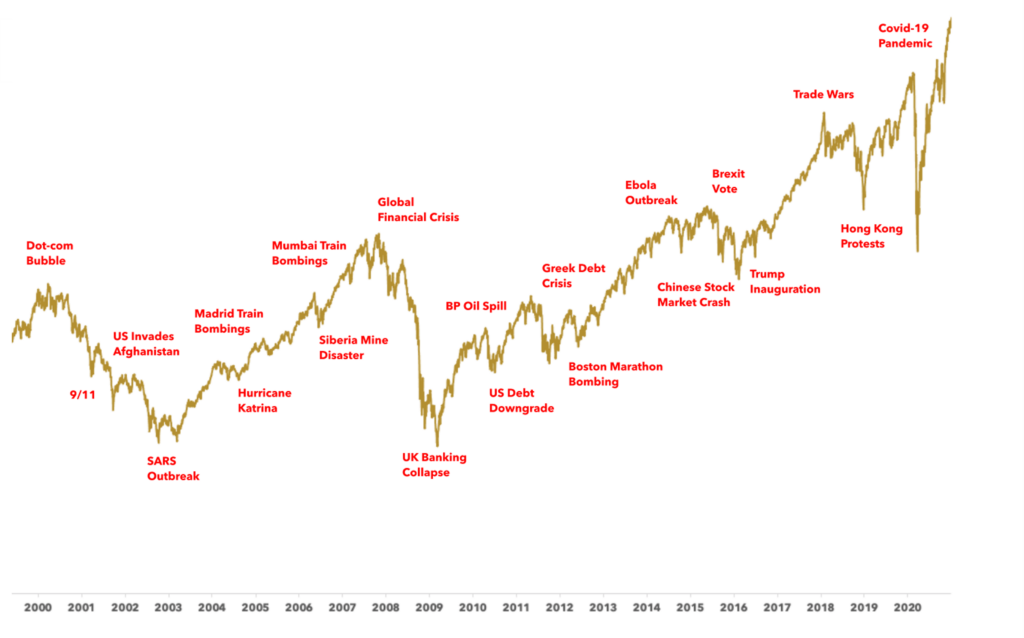

The Wall of Worry refers to a tendency in financial markets for stocks to rise in the face of seemingly insurmountable problems. However, it usually turns out that the problems are temporary and that they are eventually resolved. As seen in the chart below, history is filled with such instances whether it be the bursting of the Dot-com Bubble, the Global Financial Crisis, or the COVID-19 Pandemic.

However, as we all know, the stock market cannot climb the Wall of Worry 100% of the time. Market pullbacks and market corrections are normal, even during Bull Markets. According to Cornerstone Macro, there have been 230 corrections of 5% or more for the S&P 500 since 1928. The average duration of these corrections was 1.8 months and the average decline of these corrections was 11.9%.

The complicating factor about corrections is that nobody can predict when they will happen and nobody knows how long they will last. Having said that, we believe that investors should embrace the next correction, whenever it might happen. From our vantage point, the global economy has a lot of slack remaining from the COVID-induced recession of 2020. We believe that the global economy has more recovering to do and this is especially the case for Consumer Service sectors including restaurants, hotels, and travel related industries.

In addition to an ongoing global economic recovery, investors will soon have seasonality on their side given that the 4th quarter begins next week. According to Ned Davis Research, the median Q4 return for the MSCI World Index since 1970 has been +4.4%. This includes a return of +4.6% during secular bull markets and a return of +4.1% during secular bear markets. Over the last 50 years, the 4th quarter has been positive 83% of the time, which is a higher percentage than any other quarter of the year.

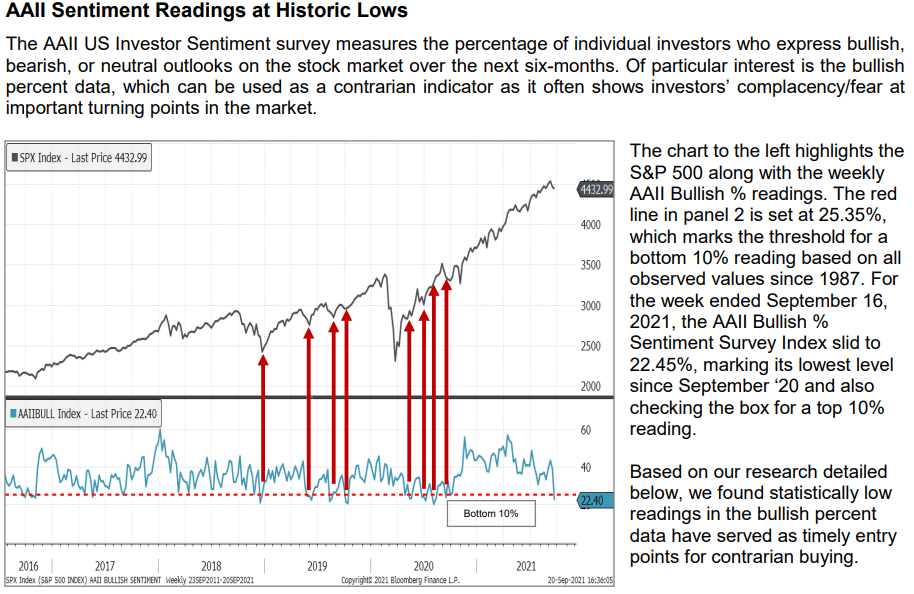

Finally, it’s worth considering some of the various Consumer Sentiment measures. Many of these measures are severely depressed and sometimes this can serve as a contrarian buying signal. For example, the American Association of Individual Investors (AAII) survey is currently at a historic low. According to Piper Sandler and as seen in the chart below, the current survey indicated a reading in the bottom 10% based on all observed values since 1987.

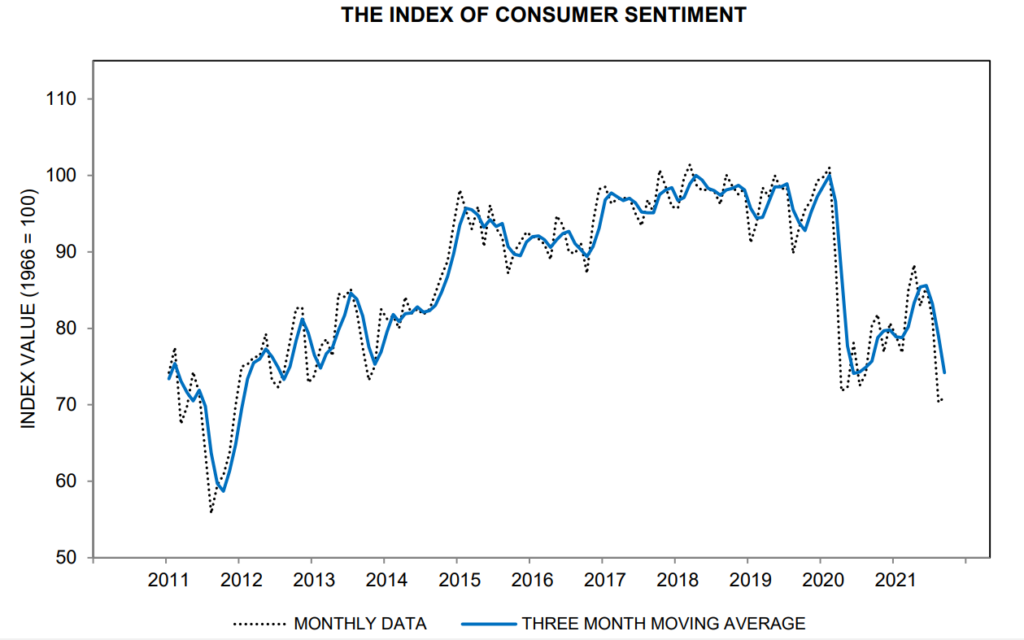

Another consumer sentiment measure is the University of Michigan Consumer Sentiment Index. This index has declined for several consecutive months as the Delta variant and higher inflation appear to have dented consumer confidence. According to Ned Davis Research and as seen in the chart below, the overall index is at its lowest level since December 2011 and in line with the level in March of 2020 during the onset of the COVID pandemic.

These Consumer Sentiment measures indicate that investors are currently very pessimistic. This implies that there is a lot of room for consumer sentiment to improve. At some point this should have positive implications for the stock market. This helps to explain why we believe that investors should embrace the next correction, whenever that might happen.

Have a good weekend,

Phil

*Cumberland and Cumberland Private Wealth refer to Cumberland Private Wealth Management Inc. (CPWM) and Cumberland Investment Counsel Inc. (CIC). NCM Asset Management Ltd. (NCM) is the Investment Fund Manager and CIC is the sub-advisor to the Kipling and NCM Funds. CIC is also the sub-advisor to certain CPWM investment mandates. This communication is for informational purposes only and is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. Reasonable efforts have been made to ensure that the information contained herein is accurate, complete and up to date, however, the information is subject to change without notice. The communication may contain forward-looking statements which are not guarantees of future performance. Forward-looking statements involved inherent risk and uncertainties, so it is possible that predictions, forecasts, projections and other forward-looking statements will not be achieved. All opinions in forward-looking statements are subject to change without notice and are provided in good faith but without legal responsibility. Past performance does not guarantee future results. CPWM and CIC may engage in trading strategies or hold long or short positions in any of the securities discussed in this communication and may alter such trading strategies or unwind such positions at any time without notice or liability. CPWM, CIC and NCM are under the common ownership of Cumberland Partners Ltd. Please contact your Portfolio Manager and refer to the offering documents for additional information.