‘Tis The Season

The Holiday season is around the corner and it couldn’t happen at a better time. A little rest and relaxation are much needed after the crazy year we have all been through!

The year started off on a positive note with the global economy in acceleration mode and global stock markets performed well out of the gate. However, by late February COVID-19 headlines created a panic that caused the S&P 500 to fall by 34% over a one-month period. After the panic subsided, stocks surged with global equity markets rising by more than 60% from the March lows.

After an unprecedented year, we hope that 2021 will represent a return to normalcy or at least something more normal than 2020. Taking a trip, eating at a restaurant, and getting together with friends & family would be nice. A return of diplomacy may also be welcomed. With Joe Biden as President, the United States should see the return of a steadier hand in the White House with a more multi-lateral approach towards foreign policy.

As 2020 nears an end, investors face several crosscurrents. On the positive side, the US election has passed with a market-friendly outcome and COVID-19 vaccines are in the process of being distributed. This type of backdrop would typically be the all-clear signal investors need to shift out of defensive work-from-home beneficiaries and into more cyclical investments. However, major developed countries across the Northern Hemisphere are facing new record levels of COVID-19 infections. This has led to a new round of economic lockdowns. It also increases the risk that some companies might not make it to the other side of this pandemic. More stimulus would help so let’s hope that recent stimulus discussions are finalized sooner rather than later.

Looking ahead to 2021 there is a consensus view that the world will stage a strong recovery. Several economists are forecasting real GDP growth of 5.0% to 5.5% for the global economy. This would represent the fastest level of growth since the 1980’s. As long as the vaccines do their job and people are willing to take them, we believe that the consensus view is achievable. Under this scenario we would expect a continuation of the rotation towards more cyclical areas of the market and better returns from the laggards as COVID losers stage a recovery. If the consensus view materializes, it should be a good year for the stock market and it would feel rewarding given what everyone has been through in 2020.

This will be our last note of the year so thank you for reading.

Happy Holidays and I wish you a healthy and prosperous year in 2021!

November – A month of Thanksgiving and a month to give thanks

November was a great month for many reasons. Not only were global equity markets exceptionally strong, but we also received promising news on 3 separate vaccines with very high effectiveness rates in the 90%+ range. It has been a challenging year but there is light at the end of the tunnel!

During the month of November, the MSCI World Index was up 12.7%. The MSCI World Index is a very broad index which includes more than 1,500 companies across 23 developed markets so it’s a great proxy for what’s going on in global stock markets. The 12.7% gain did not break the all-time monthly record, but it’s pretty darn good when you consider that it’s a larger return than what is typically generated over a 12-month period! The pan-European Stoxx 600 index, meanwhile, notched its best-ever month in November, ending 13.7% higher. The major U.S. indexes also generated strong returns in November with the S&P 500 rising 10.8% and the Dow Jones Industrial Average gaining 11.8%. This was the largest monthly gain for the Dow Jones since 1987. Technology stocks also had a great month with the Tech-heavy Nasdaq Composite Index rising 11.8%.

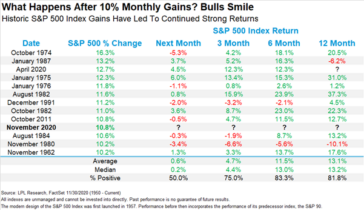

So after an amazing month, what are we going to get for an encore? While nothing is guaranteed, history does paint an encouraging picture. Over the last 60 years, periods of strong market gains have often been followed by further gains as seen in the chart below. According to LPL Financial, following a 10% monthly gain, the S&P 500 is up 83% of the time 6 months later by an average 11.5%. On a 12-month horizon, the S&P 500 is up nearly 82% of the time by an average 13.1% following a monthly gain of 10%.

Over the last 8 months stock market returns have been so strong that they have surpassed the expectations of almost every expert on Wall Street and Bay Street. How can we put this into perspective and how can it be explained? Nobody has the exact answer, but from our vantage point the strong gains can be partly explained by a forward-looking stock market and sidelined cash getting put to work. Notwithstanding a major shock or a vaccine failure, the global economy is set for a significant recovery in 2021 and so the market has strengthened in advance of the recovery. In addition, it also looks as if investors who sidelined trillions of dollars of cash have grown tired of making modest returns in money markets funds and have decided to move into equities.

Following this huge advance in global equity markets, a common question we now hear is “is it too late to get in?”. The answer of course, is, it depends. It depends on who is asking the question, their tolerance for risk, and their investment time horizon. From our perspective, we see an economic recovery and the potential for a sustainable economic expansion driven by a synchronized global recovery.

But what about valuations? Stocks look expensive on several measures that compares them with their own sales, book values, or earnings. However, the yields on U.S. Treasury bonds hit an all-time low earlier this year and remain at levels that most experts would not have predicted 5 or 10 years ago. All else equal, lower interest rates should justify paying more for stocks given that equities can be discounted at a lower rate, making them more valuable.

Recent findings by American economist Robert Shiller shed some light on this subject. Mr. Shiller is well respected on Wall Street given that he famously predicted the Technology meltdown in 2000. He also predicted the 2007 stock market decline that was triggered by the crash in US housing. In a recent publication, Mr. Shiller discusses the surprising resilience of global equity markets in the face of the COVID-19 pandemic. In his piece, he suggests that perhaps investors shouldn’t be so surprised by the market’s resilience. In his opinion, a close look at a measure he calls the Excess CAPE Yield (ECY) puts the long-term outlook for global stock markets in better perspective. The Excess CAPE Yield measure is a useful way to think about long-term valuations for stocks in way that also incorporates the current level of interest rates.

To calculate the Excess CAPE Yield (ECY), one must take the inverse of the cyclically adjusted PE ratio to get a yield and then subtract the ten-year real interest rate. A higher measure indicates that equities are more attractive. The ECY in the US, for example, is 4%, derived from a CAPE yield of 3% and then subtracting a ten-year real interest rate of -1.0%.

According to Mr. Shiller, the Excess CAPE Yield has typically done a good job of predicting subsequent returns over the following 10 years. As seen in the chart below, the Excess CAPE Yield in the US is just slightly below the average of the last 100+ years. According to Mr. Shiller, this suggests that U.S. stocks should generate real returns of approximately 5% per year over the next decade.

Source: Bloomberg

Outside of the US, Mr. Shiller found some very striking results. The Excess CAPE Yield is close to 40-year highs across several global regions and is at all-time highs for both the UK and Japan. The Excess CAPE Yield for the UK is almost 10%, and around 6% for Europe and Japan. China’s ECY is at about 5%. All of these figures indicate that worldwide equities are highly attractive relative to bonds right now.

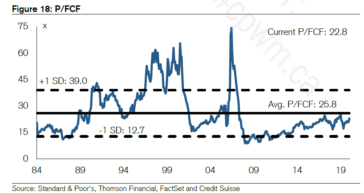

Another measure that suggests that equities are attractive is the price-to-free cash flow measure. Free cash flow is one of the key determinants for valuing stocks so this is a highly relevant measure. As seen in the chart below, the price-to-free cash flow ratio has averaged 25.8x over the last 35 years. This ratio is currently sitting at 22.8x, which implies that the current price-to-free cash flow ratio is 11.6% below the average of the last 35 years.

Taking everything into consideration we remain cautiously optimistic as we approach the end of 2020 and as we look ahead to 2021.

Have a good weekend,

Phil

“Buy low/sell high” is tough when you’re not sure which way is up

It’s probably the first adage one ever hears about investing which sounds easy enough. But in the rapidly shifting world of the markets, buying low and selling high isn’t nearly as easy as it appears.

When markets are down, investors believe that risk is elevated. In fact, risk is reduced since the ‘sold-down’ markets include a “fear premium” or discount -prices drop as events happen not after they occur, investors shouldn’t fear further losses once prices have hit bottom. Another adage, “If it’s in the press, it’s in the stock price”, rings true.

When the markets react, a move up or down factors in the past. Environments investors perceive as risky and volatile are less risky because prices have already dropped and will rise again as history reveals.

To execute, one needs knowledge and experience to recognize when a market move is just a temporary ‘blip’ that’s here today and gone tomorrow, versus when it could be the first reverberations of a trend for the months, possibly years ahead.

Knowing what to look for and having the skill and confidence to select opportune investments are two different things. Younger generation investors may be unsure, but those who have gone through the tough times and understand the paradox of investing, will be able to both pull the trigger and recognize danger signs.

Regardless, investing in the market requires a solid plan. All investors need to understand their end goals, the risks they can take and go from there with a team of active managers on their side.

Investing Between a Rock and a Hard Place

Being stuck between a rock and hard place is never a fun place to be. When the rock is a rising interest environment and the hard place is a volatile stock market, trying to save for retirement can be a challenge.

Investing with Discipline

While your professional success is unquestionable, have you applied the same skill, discipline and perseverance to managing your investments?

Investment Insights from our CIO

Is the volatility we’ve seen in the market so far this fall set to continue? A closer look at key indicators will help determine what can happen.

Following the FED rate hike on September 26th market volatility began to accelerate, however the S&P 500 index remains at less than 6% off its all-time highs, the TSX is looking attractive from a valuation perspective and there has been little impact on corporate bond spreads.

Today’s Landscape and Opportunities in Canadian Pipelines and Midstream Companies

The S&P/TSX Oil & Gas Storage and Transportation Total Return Index is down approximately 14.7% year-to-date (through April 26). Rising interest rates, larger than normal discounts for western Canadian natural gas and crude oil (particularly heavier crude oil), and various delays with new projects have all given analysts, pundits, and the media plenty of material to construct a negative narrative.

This article appeared in the Spring 2018 issue of our newsletter, “Interest Gained”. To read the full newsletter, please click here.

Changing of Chairs: Styles of Central Banker and Rate Cycles

Since the mid 70s the Chairman of the Federal Reserve Board have served at least two consecutive terms (terms are 4 years at a time). The appointment of Janet Yellen, being the first women Chairperson of the Federal Reserve Board, back in 2014 by Barack Obama marks the first break in that trend, serving only one term. Many have asked if this change in Chairs will make a difference in the interest rate hike cycle in the US. Our Short answer: NO.

This article appeared in the Spring 2018 issue of our newsletter, “Interest Gained”. To read the full newsletter, please click here.

US Election Cheat Sheet

Chairman Gerry Connor in conjunction with Sukyong Yang, Lead Manager Global Equities, have prepared an informal briefing or “Cheat Sheet” on the possible outcomes of the US election. While there are many unknowns and variables, we hope this summary will provide relevant perspectives and our insights.

Our Initial Perspectives on The Brexit Vote

The Brexit referendum answered one question but raised a number of complex issues. In their respective commentaries, Lead Strategist, Gerald Connor, CIO, Peter Jackson and Global Equities PM, Sukyong Yang review their perspectives on this significant outcome and the impact it could have at this early stage.

While all three commentaries share commonalities, they also focus on different key elements. Click on the links below to read more.