A novel approach to funding your RESP

When life moves, your money moves. When you have a child, life starts moving. This article provides an overview of the Registered Education Savings Plan (RESP), an excellent tool to save for a child’s education. It explains the three phases of RESP planning and shares a novel approach to funding your RESP that could potentially accelerate its benefits.

The strategies discussed here may or may not be directly applicable to your wealth plan. But if saving for a child’s post-secondary education is in your plan, there’s no denying that an RESP can play a vital role.

A review of RESP basics

RESPs are designed to help parents save for their children’s post-secondary education at a university, college, trade school, or technical school in Canada or abroad. Contributions to the account grow on a tax-sheltered basis until withdrawals are made to support post-secondary education expenses. A unique feature of RESPs is that our federal government matches a portion of the funds contributed.

RESP Account Types

There are Family Plans and Individual Plans. A Family Plan consists of multiple qualified beneficiaries, who are children related by blood or adoption. An Individual Plan is for a single beneficiary. Family Plans offer more flexibility since the contributions, government grants, and growth of the investments can be shared between beneficiaries.

Who can open a RESP?

Anyone can open an RESP, including parents, grandparents, relatives, friends, or guardians. These are known as “subscribers.” It is generally best to open RESPs in the joint names of the beneficiaries’ parents and have others contribute to those RESPs. This can help avoid accidental over-contributions and also provide the most flexibility if a child does not pursue post-secondary education.

Contributions and grants

There is no annual RESP contribution limit, but there is a lifetime maximum contribution limit of $50,000 per beneficiary. RESP contributions are not tax deductible, but they attract a government grant known as the Canadian Education Savings Grant (CESG) equal to 20% of annual contributions, up to $2,500 per year and $7,200 per beneficiary over their lifetime.

The CESG is a federal program. British Columbia and Quebec also offer provincial programs that could be worth up to $1,200 and $3,600 respectively.

Phase one: Accumulation

The first phase of an RESP is all about making contributions, earning grants, and accumulating money. Due to the long-time horizon associated with RESPs, investment strategies focused on growth are generally the most suitable. But as in all investing, it is important to remain within your comfort level and risk tolerance.

The power of tax-sheltered compound growth

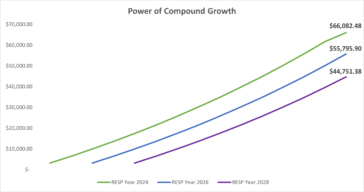

A key advantage of RESPs is being able to compound your investment and earn returns within a tax-sheltered environment. And, like all compounding, the sooner you start the better. The graph below compares what would happen if you started investing in 2024, 2026 or 2028 based on annual contributions of $2,500, an annual CESG of $500, and annualized investment growth of 5%.

If you start in 2024, the account will be worth just over $66,000 when the beneficiary turns 15 in 2038. This is $10,000 more than if you delayed two years and $20,000 more than delaying contributions for four years.

A novel approach: pre-funding your RESP

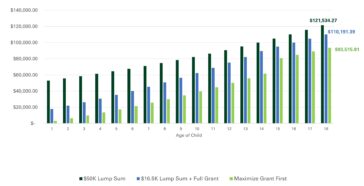

Since there is no annual contribution limit for RESPs, you can pre-fund your account and have more tax-sheltered money growing for longer. The extreme case would be contributing the full $ 50,000-lifetime limit all at once. In this scenario, you would maximize the amount of money that is able to grow in the plan and receive one $500 CESG payment for the initial contribution but sacrifice the remaining $6,700 in grants.

However, if you wanted to boost your tax-sheltered growth and also receive the maximum CESG, you could contribute $16,500 in year one and then contribute $2,500 annually until the $ 50,000-lifetime limit is reached. This mix of contributions will allow you to claim the maximum CESG of $7,200.

The graph below illustrates three scenarios: $50,000 all at once versus $16,500 in year one followed by $2,500 annually versus $2,500 annually and a final top-up in year 15. All three scenarios assume 5% annualized investment growth.

In this illustration, the $50,000 upfront contribution results in the highest end value. More money compounding for a longer period more than compensates for the government grants that were sacrificed. However, there is a caveat: this illustration assumes a level 5% annualized rate of return, and returns are more variable in the real world. This strategy could underperform if there is a period of lower investment performance, or outperform by an even greater margin if returns are higher.

Pre-funding strategies should be assessed in terms of your overall financial priorities, wealth, and life objectives. While post-secondary education is important, other financial commitments or strategies may need to be prioritized if excess funds or cash flow are available.

For the more risk-tolerant, making larger initial deposits may be appropriate. For the more risk-averse, making an initial $16,500 contribution followed by regular contributions to maximize the government grant may be more suitable.

Phase two: Transition

The transition phase is the 3 years leading up to the start of post-secondary education. During this period, you will want to assess the likelihood of your child attending a post-secondary education program, identify other sources of funding if your RESP alone is insufficient, and de-risk your investments as the withdrawal date gets closer

What if you child is not pursuing post-secondary education?

If you have a Family Plan with more than one child named as a beneficiary, you can use the RESP to support your other children’s post-secondary education plans. In a Family Plan CESG, contributions and growth can be shared between family members within certain limits.

If none of your children attend post-secondary education, you can withdraw your contributions and return the grants to the government, however, the growth of the RESP could be taxed at your marginal rate plus a 20% penalty. The way to avoid this tax is to transfer the RESP growth to your RRSP, provided that you have enough RRSP contribution room.

This scenario highlights the importance of naming both parents as joint subscribers to the RESP. If correctly timed, a couple can greatly reduce the amount of RESP growth that could be taxed and penalized. And, if some RESP growth needs to be included as income for tax purposes, you have two incomes to spread the tax over.

When the RESP isn’t enough: Other income sources

RESPs are rarely enough to cover all of a child’s post-secondary education expenses. When the start of the program nears, it is important to evaluate the potential expenses in comparison to your RESP value. If extra funds are required, you can start to plan their potential sources. This could be from your cash flow or savings (TFSAs or non-registered accounts are best).

De-risking your investment strategy

A sharp drop in your RESP’s value just when you need to start making withdrawals is a risk you want to minimize. Options to consider are shifting a year or two worth of expected expenses to cash, or changing your investment strategy to be more conservative overall. With a Family Plan, it’s wise not to get too conservative too quickly, as there are multiple beneficiaries to consider and a need to balance current and future needs.

Phase three: Withdrawal

The withdrawal phase is when you actively withdraw funds from the RESP to support post-secondary education expenses. This phase is all about taxation.

There are two types of RESP withdrawals, non-taxable withdrawals consisting of your contributions, and taxable withdrawals consisting of CESG and accumulated growth. The taxable withdrawals can be attributed to the beneficiary or to the subscriber.

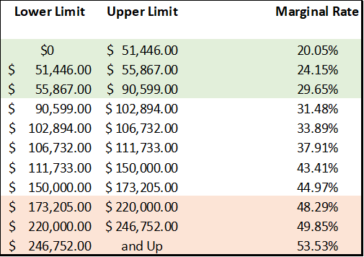

To maximize the benefit of the RESP, you want to prioritize having taxable withdrawals attributed to beneficiaries, since these amounts will be included in their income and taxed at much lower marginal rates. This can be seen in the table below showing the combined Federal and Ontario Tax brackets for 2024.

There is also the Basic Personal Amount to consider, which is the amount of income that can be earned before any tax has to be paid. For 2024, this amount is $15,705, which means that if the child has no other income, they can take $15,705 from their RESP tax-free to cover education expenses.

It is also important to prioritize taxable withdrawals early to ensure all the CESG that has been received is paid out. If it has yet to be fully paid out by the time beneficiaries have finished post-secondary education, it will be returned to the government.

Another helpful tax tool is the Tuition Tax Credit. This is a non-refundable tax credit available for post-secondary students. The credit is equal to 15% of “eligible tuition and fees”. These amounts are usually provided by the post-secondary institution. Unused credit can be carried forward to future years or transferred to a parent.

Key RESP points to remember

- When you contribute to an RESP, you receive a 20% grant from the federal government. The more you contribute and the sooner, the greater the benefits of tax-sheltered compound investment growth.

- When post-secondary education nears, plan to de-risk your investment strategy and consider additional ways to pay for education expenses. If your child is unlikely to pursue post-secondary education, it’s time to implement a backup strategy.

- When it’s time to start withdrawing from the RESP, aim to have them taxed in your child’s name while he or she has little or no other income to maximize the after-tax benefits of the RESP.

If you have questions about the best RESP strategies and approach for your specific situation, a Cumberland Portfolio Manager is available to assist you. We seek ways to optimally integrate education savings goals with a family’s overall wealth management plan.